Strategy Formulation and Sustainability Performance of Bumiputera Construction Companies: A Conceptual Paper

Abstract

Sustainability performance is a rapidly developing field of research. However, there are few studies and practices on the sustainability performance of construction companies, namely Bumiputera construction companies. Although some scholars have conducted studies in the various sectors of the economy, which suggest that companies that adopt sustainability practices have some advantages, the process of promoting sustainability in the Malaysian construction industry is generally slow. Therefore, there is a need to encourage these companies to adopt sustainability practices so that they can achieve better financial performance in the long run. This paper proposes a research framework that considers the role of strategy formulation and firm size as moderating variables in the relationship between strategy formulation and corporate sustainability performance of Bumiputera construction companies in Malaysia. The objective of this paper is to provide a literature review on the effects of strategy formulation and firm size on the sustainability performance of Bumiputera construction companies in Malaysia. This study will contribute to new knowledge on the sustainability performance of Bumiputera construction companies and will also have an impact on the various stakeholders in the construction industry, especially on Bumiputera construction companies in terms of their competitiveness and sustainability performance.

Keywords: Construction industry, strategy formulation, firm size, corporate sustainability performance

Introduction

The construction business is tough, even though it is easy to register as a builder in Malaysia. Theiencouraginginumberiofiactivitiesiinitheiconstructioniindustry has increased the number of contractors and construction workers (CIDB, 2019). According to the CIDB, as of July 2022, a total of 130,751 construction companies (Class G1 to G7) were registered in Malaysia, i.e., an increase from 104,858 companies in 2019. Of the total registered companies, 70,579 are Bumiputera construction companies, representing 53.98 per cent of all construction companies that have been registered by the CIDB (CIDB, 2022). Construction is one of the most difficult businesses of all and it takes a long time to produce capable contractors (Koon, 2013). Bumiputera construction companies often fail because they do not fully understand the construction process and what is needed to succeed. This is because most Bumiputera contractors have not received training in the construction industry, and therefore do not have the necessary knowledge to ensure the success of projects while meeting specifications and costs (Fadzil et. al.., 2017). The Malaysian governmentihasilaunchediseveraliprogrammesitoisupportitheiBumiputera contractors, including the New Economic Policy (NEP), the Bumiputera Economic Transformation Roadmap (BETR), and others. However, Bumiputera construction companies are still unable to succeed due to a lack of skills, knowledge, tendering methods, financial problems, and low labour productivity. Correspondingly, the constant awarding of contracts to Bumiputera without conducting a tendering process only makes them more incompetent. The construction business is an unpredictable and complex environment where players need to be dynamic and resilient to survive in the long run.

Literature Review

Construction industry

The construction industry is highly competitive and volatile. According to Mulcahy (1990), in order to survive, construction companies must have a clear goal and know where they want to go, how to get there, and how to remain there. Thus, a thorough plan is needed to steer the company in the right direction. Respectively, Thomson et al. (2001) have explained that strategic planning is a set of decisions and actions that lead to the formulation, implementation and control of strategies to achieve the company's goal. However, strategic planning is not widely used in the construction industry as it is considered to be lengthy and costly. Earlier, Betts and Ofori (1992) pointed out that the construction industry began to use strategiciplanningiasiaimeansiofilong-termisurvivaliinithei1990s. Omar and Azmi (2015) have also noted that construction business failure is common in the construction industry. Significantly today’s business climate is dynamic and constantly evolving; to be competitive and to stay in the business companies need to constantly adapt. Ramli (2017) has mentioned that although the Malaysian government has made great efforts to promote Bumiputera entrepreneurship, the number of Bumiputera companies is not growing at the same pace as economic progress. Notably, many problems are related to the development of Bumiputera entrepreneurship. He has also noted that the Malay Bumiputera in particular are still lagging behindiinitheimodernieconomicisectoriwhileifacingichallengesithat led to their failure in the early years of their business. Several variables influence the sustainability of Bumiputera construction companies; their actions affect the social and environmental sustainability of the sector, which in turn affects the economic sustainability of the sector.

Corporate sustainability performance

Recently, we have noticed that sustainability and sustainable development are gradually becoming more important in all sectors worldwide. The construction industry is no exception. Construction activity has a significant impact on the social, environmental and economic aspects of sustainability. Similar to other sectors, the construction industry is increasingly recognising the importance of sustainable construction practices, which leads to a commitment to sustainable practices at all stages of a construction project, i.e., design, construction and operation. In Malaysia, the concept of corporate sustainability practices is still adopted on a voluntary basis (Mdolo et al., 2018; Zahid & Ghazali, 2017). Given the importance of sustainability, several Malaysian organisations actively promote it through various strategies, toolkits, guidelines, initiatives and policies (Muhammad Kashif et al., 2019). Corporate sustainability performance can also be considered as a company's survival strategy (Hu & Karbhari, 2015; Lloret, 2016). In its most basic form, corporate sustainability performance encompasses business continuity, but occasionally ignores other stakeholders such as the environment and society (Mdolo et al., 2018). In reality, sustainability can be achieved through the management of economic, natural and social capital (Dyllick & Hockerts, 2002). Table 1 describes the individual elements of corporate sustainability performance.

Strategy formulation

Strategic planning is considered a critical element of business management in creating corporate sustainability and competitive advantage (Chaudhry et al., 2012). The concept of 'sustainability of a construction company' can be defined as the ability of a company to operate effectively and meet its obligations under the changing conditions of the competitive market environment and uncertainty of construction volume (workload) (Lapidus & Abramov, 2018). In addition, Al-Ghrairee (2021) has noted that it is crucial to focus on the role of strategic planning in construction companies as the construction industry is key to the country's economic growth and long-terminational socio-economic development. Tarifi (2021) has stated that strategic planning is critical to the management of an organisation as it guides the organisation in determining strategic plans to be used by the organisation. Correspondingly, Shrivastava (1995) mentioned in his studies that an organisation's sustainability initiatives and its corporate strategy must be closely connected and not managed independently as separate programmes. The process of strategic planning can be divided into three main areas: Strategy Formulation, Strategy Implementation, and Strategy Evaluation and Control.

According to Pearce and Robinson (2009), strategy formulation is a guide for managers to help them determine the scope of their organisation's activities, the goals they will pursue and the tools they will use to achieve those goals. The organisation develops strategies to achieve a variety of goals, including overcoming external forces, exploiting opportunities, overcoming significant challenges, meeting stakeholder expectations (Johnson et al., 2008), and gaining a competitive advantage (Hill & Jones, 2012; Porter, 1998) as well as developing the organisation's resources and competencies (Hamel & Prahalad, 1994). The way an organisation formulates its strategy has become one of the most heated debates in the field of strategic management. The traditional view is that strategy formulation is primarily the result of a methodical, logical planning process by a senior management team, which is then passed on to the business for implementation. This approach is often implemented in large companies through a formal strategic planning system (Gimbert et al., 2010). Formulating a strategy is also about determining where you are now, where you want to go and how you are going to get there. This includes a situation analysis, a self-assessment, and an analysis of competitors inside and outside the company, as well as setting goals to go along with the assessment. This process is critical to the success of a company as it provides a framework for the actions that will lead to an expected outcome. The process of strategy formulation requires the involvement of several levels of management. Mintzberg and Waters (1985) point out that anyone in the organization who happens to have control over important or directional actions can be a strategist. Pitts and Lei (2000) emphasise that the responsibility for strategic management lies with the top managers because it involves significant financial expenditure, has long-term implications and often generates controversy. Therefore, for this study, the main problems in strategy formulation need to be examined and analysed.

Firm size

In addition to strategy formulation, several other variables influence the sustainability of Bumiputera construction companies. Construction companies have special characteristics as they operate in a fragmented and project-based industry (Giritli & Oraz, 2004). Empirical evidence suggests that organisational characteristics and strategies are related to the firm’s performance. However, the impact on performance is complex, with some studies finding a positive or direct relationship, while others report a negative or indirect relationship (Lavie, 2006; Nandakumar et al., 2011; Pertusa-Ortega et al., 2010). Firm size is defined as the number of employees in the organisation (Ainuddin et al., 2007; Hashim et al., 2007; Ling et al., 2007; Yoon & Suh, 2019). Certain structural characteristics of organisations, such as their size, have been recognised in studies in measuring their performance (Yoon & Suh, 2019). The size of aniorganisation has been highlighted as a crucial element that influences numerous aspects of its structure (Donaldson, 2006). According to Panda (2020), there are several definitions of firm size in business. The most widely used definition is the number of employees Asian indicator of the firm’s size, while some use net assets, the annual turnover, and for some the amount of invested capital to measure a firm’s size. However, some companies also use their net assets, annual turnover and even the amount of investment in plant and machinery as the determinants of firm size. The classification of firm size by many management authors is not relative when it comes to the operations of a construction company.

Pearce et al. (1987) identify the impact of firm size on the relationship between planning and performance as a key operational challenge. The study argues for a more specific investigation focusing on firm size, particularly how this variable interacts with the dimension of formality. Size has been suggested as an important element of contingency that should be considered in the development of effective strategic planning systems (Lenz, 1981; Lindsay & Rue, 1980). It can also be argued that the strategic planning system in a large company serves as a coordination tool to integrate and control the different aspects of the company. Glaister et al. (2008) in their study of 500 large firms in Turkey have found that firm size has a moderating effect on the firm’s performance that is positively associated with formal strategic planning. For the purpose of this study, firm size is determined by the contractor's CIDB classification, number of employees, profit or turnover, and net assets. At the same time, the number of employees indicates whether the company is small, medium or large (Table 2).

Method

Desk research has been employed in this research whereby references are based on previous research, published reports and statistics that are related to corporate sustainability performance and strategy formulation of construction companies. A keyword of corporate sustainability performance, construction companies and firm size have been used in the literature search.

Findings

In reviewing the literature, a number of issues were identified in relation to the research topic. The first is the lack of studies on the sustainability performance of Bumiputera construction companies in Malaysia, as most previous studies have mainly focused on listed companies in developing countries, such as Malaysia (Abdul Aris et al., 2016). Although some scholars have conducted studies in various sectors of the economy-iwhich suggest that companies that adopt sustainability practices have some advantages (Khaveh et al., 2012; Konar & Cohen, 2001), the process of promoting sustainability in the Malaysian construction industry is generally slow (Shafii et al., 2006). By encouraging these organisations to adopt sustainability practices, companies can achieve better long-term financial performance, focusing on both non-financial and financial performance (Chong et al., 2018). Despite improvements in the adoption of sustainability practices, Malaysian companies' performance has stagnated (Zahid & Ghazali, 2017).

The second issue that has been identified is the lack of studies on the impact of strategy formulation on the sustainability performance of Bumiputera construction companies. Different researchers have looked at strategic planning in a company from different perspectives. The construction sector, like all other businesses, is facing increasing competition in its business environment (Balatbat et al., 2011). They are currently struggling to stay afloat in an ever-changing business climate which includes the problem of not being competitive and being constrained in their ability to expand in the business sector (Sabiu et al., 2017; Yesil & Kaya, 2013). Despite numerous aids, support and concerns in expanding the entrepreneurial agenda of Bumiputera in the country, their growth has fallen short of expectations (Sabiu et al., 2017). Moreover, strategic planning is considered a critical component of organisational management in creating corporate sustainability and competitive advantage (Chaudhry et al., 2012). The importance of strategic planning and its relationship to organisational success has produced mixed results (Jayawarna & Dissanayake, 2019). There is a large and growing literature on the ability of different strategic planning processes to create a competitive advantage for companies (Pearce & Robinson, 2009).

The third issue that has been identified is that there is no study that has thoroughly analysed the three aspects of the sustainability performance of construction companies, namely economic, environmental and social sustainability performance (Chang et al., 2018). According to a survey conducted by Zainul Abidin (2009), companies in Malaysia are aware of sustainable concepts but are not willing to change their business practices to implement sustainable practices. This is because most of them believe that sustainable strategies would only increase costs instead of helping the business to maintain and increase profits (Panda, 2020). Moreover, many believe that sustainability is only about saving the environment without realizing that sustainability is also about balancing the other two elements, namely the social and the economic (Zainul Abidin, 2009). Moreover, issues of corporate sustainability have become a focus of research, as companies are a valuable source of revenue and play an important role in helping the world achieve a sustainable agenda (Chang et al., 2018). There is limited research that addresses the economic, environmental and social components of sustainability (Chang et al., 2018). Most of the research to date focuses on identifying best practices to improve environmental performance without considering other dimensions of corporate sustainability (Chang et al., 2018; Zhang et al., 2018).

Finally, the fourth issue that has been identified is the lack of study on the influence of firm size on the sustainability performance of construction companies. Construction companies have special characteristics as they operate in a fragmented and project-based industry (Giritli & Oraz, 2004). Langford and Male (2001) have found that the operating environment of small construction firms differs from that of medium and large firms in a number of factors that are reflecting the nature of the underlying power base, the nature of the client base and the firm’s stock of strategic assets. Pearce et al. (1987) identify the impact of firm size on the relationship between planning and performance as one of the key operational challenges. This study argues for a more specific study, focusing on firm size, particularly how this variable interacts with the formality dimension. Empirical evidence suggests that organisational characteristics and strategies are related to firm performance. However, the impact on performance is complex, with some studies finding a positive or direct relationship, while others report a negative or indirect relationship (Lavie, 2006; Nandakumar et al., 2011; Pertusa-Ortega et al., 2010).

Discussion and Conclusion

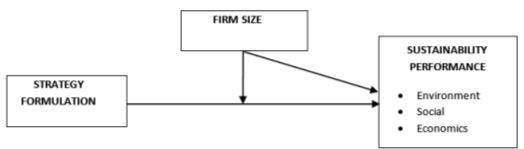

According to the literature reviewed above, this study examined the impact of strategy formulation on the sustainability performance of Bumiputera construction companies in Selangor and the role of firm size in moderating the relationship between strategy formulation and sustainability performance, as is shown in Figure 1.

The number of studies on corporate sustainability performance is growing and the expansion of knowledgeihasiattractediailargeinumberiofischolarsifromidifferent fields. Based on the literature review, previous studies have mostly focused on the problems and issues of Bumiputera construction companies, their financial performance, and the competitiveness in the construction industry (Ahmad et al., 2018; Halim et al., 2014; Omar & Azmi, 2015; Othman, 2010; Rahman & Rahmat, 2016; Serpell et al., 2013; Sukur et al., 2018). There is little research on the overall sustainability performance of Bumiputera construction companies and the factors that ensure sustainable business performance. Therefore, this is a timely study to examine the impact of strategy formulation and the firm size of Bumiputera construction companies on their long-term survival in the construction sector. It is expected that this study will benefit Bumiputera construction companies and help them to improve, grow, survive and strengthen their capabilities in the construction sector in the long run. This is also in line with the government's initiative to introduce sustainable practices and expand knowledge content to transform the construction sector and strengthen economic growth.

References

Abdul Aris, N., Othman, R., Abdul Rahman, S., Madah Marzuki, M., & Wan Chik, W. (2016). Ethical Codes as Instruments for Cooperative Sustainability. Social and Management Research Journal, 13, 29-44. DOI:

Ahmad, H. N., Amran, N. A., & Arshad, D. A. (2018). Financial Issues in a Bumiputera Small and Medium Enterprise (SME). International Journal of Economic Research, 14, 199-207.

Ainuddin, R. A., Beamish, P. W., Hulland, J. S., & Rouse, M. J. (2007). Resource Attributes and Firm Performance in International Joint Ventures. Journal of World Business, 42(1), 47-60. DOI:

Al-Ghrairee, L. (2021). Strategic Planning in the Construction Companies in Oman. International Journal of Research in Entrepreneurship & Business Studies, 2(1), 29-40. DOI:

Aras, G., Tezcan, N., & Furtuna, O. K. (2018). Multidimensional Comprehensive Corporate Sustainability Performance Evaluation Model: Evidence from an Emerging Market Banking Sector. Journal of Cleaner Production, 185, 600-609. https://doi.org/DOI:

Balatbat, M. C. A., Lin, C. Y., & Carmichael, D. G. (2011). Management Efficiency Performance of Construction Businesses: Australian Data. Engineering, Construction and Architectural Management, 18(2), 140-158. DOI:

Betts, M., & Ofori, G. (1992). Strategic Planning for Competitive Advantage in Construction. Construction Management and Economics, 10(6), 511-532. DOI:

Chang, R.-D., Zuo, J., Zhao, Z.-Y., Soebarto, V., Lu, Y., Zillante, G., & Gan, X.-L. (2018). Sustainability Attitude and Performance of Construction Enterprises: A China Study. Journal of Cleaner Production, 172, 1440-1451. https://doi.org/DOI:

Chaudhry, I. S., Ali, S., Fareed, G., & Fakher, A. (2012). Role of strategic planning in small business: An overview. International Journal of Management, IT and Engineering, 4(1), 316-324.

Chong, L.-L., Ong, H.-B., & Tan, S.-H. (2018). Corporate Risk-Taking and Performance in Malaysia: The Effect of Board Composition, Political Connections and Sustainability Practices. Corporate Governance: The international journal of business in society, 18(4), 635-654. DOI:

CIDB. (2019). Statistik Bilangan Kontraktor Yang Mempunyai Sijil Taraf Bumiputera (STB) Mengikut Gred Dan Negeri. https://www.data.gov.my/data/ms_MY/dataset/statistik-bilangan-kontraktor-yang-mempunyai-sijil-taraf-bumiputera-stb-mengikut-gred-dan-negeri/resource/887f2007-a3694477-a5d2-fabab436cc11

CIDB. (2022). http://cims.cidb.gov.my/smis/regcontractor/reglocalsearchcontractor.vbhtml

Donaldson, L. (2006). The Contingency Theory of Organizational Design: Challenges and Opportunities. In Organization design (pp. 19-40). Springer. DOI:

Dyllick, T., & Hockerts, K. (2002). Beyond The Business Case for Corporate Sustainability. Business Strategy and the Environment, 11(2), 130-141. https://doi.org/DOI:

Fadzil, N. S., Noor, N. M., & Rahman, I. A. (2017, November). Need of risk management practice amongst bumiputera contractors in Malaysia construction industries. In IOP Conference Series: Materials Science and Engineering (Vol. 271, No. 1, p. 012035). IOP Publishing. DOI:

Gimbert, X., Bisbe, J., & Mendoza, X. (2010). The Role of Performance Measurement Systems in Strategy Formulation Processes. Long Range Planning, 43(4), 477-497. DOI:

Giritli, H., & Oraz, G. T. (2004). Leadership Styles: Some Evidence From the Turkish Construction Industry. Construction Management and Economics, 22(3), 253-262. DOI:

Glaister, K. W., Dincer, O., Tatoglu, E., Demirbag, M., & Zaim, S. (2008). A Causal Analysis of Formal Strategic Planning and Firm Performance: Evidence From an Emerging Country. Management Decision, 46(3), 365-391. DOI:

Goel, P. (2010). Triple Bottom Line Reporting: An Analytical Approach for Corporate Sustainability. Journal of Finance, Accounting & Management, 1(1).

Halim, M., Osman, A., & Amlus, M. (2014). Determining the financial performance factors among Bumiputera entrepreneurs in Malaysian construction industry. Australian Journal of Basic and Applied Sciences, 8(12), 18-24.

Hamel, G., & Prahalad, C. K. (1994). Competing for the future. Harvard business review, 72(4), 122-128.

Hashim, M. K., Zakaria, M., & Malaysia, U. (2007). Exploring Strategic Thinking Practices Among Malaysian SMEs. Malaysian Management Review, 42(1), 29-41.

Hill, C. W., & Jones, G. R. (2012). Strategic Management: An Integrated Approach (10 ed.). Cengage Learning.

Hu, Y. Y., & Karbhari, Y. (2015). Incentives and Disincentives of Corporate Environmental Disclosure: Evidence From Listed Companies in China and Malaysia. Thunderbird International Business Review, 57(2), 143-161. DOI:

Jayawarna, S., & Dissanayake, R. (2019). Strategic Planning and Organization Performance: A Review on Conceptual and Practice Perspectives. Archives of Business Research, 7(6), 155-163.

Johnson, G., Scholes, K., & Whittington, R. (2008). Exploring Corporate Strategy: Text and Cases. Pearson Education.

Khaveh, A., Nikhasemi, S. R., Haque, A., & Yousefi, A. (2012). Voluntary Sustainability Disclosure, Revenue, and Shareholders Wealth-A Perspective From Singaporean Companies. Business Management Dynamics, 1(9), 06-12. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2071275

Konar, S., & Cohen, M. A. (2001). Does The Market Value Environmental Performance? Review of economics and statistics, 83(2), 281-289. DOI:

Koon, Y. Y. (2013). Producing competitive bumiputera contractors. https://www.malaysiakini.com/letters/223247

Langford, D., & Male, S. (2001). Strategic Management in Construction. Wiley. DOI:

Lapidus, A., & Abramov, I. (2018). Studying The Methods for Determining and Maintaining Sustainability of a Construction Firm. MATEC Web Conference, 251, 6. DOI:

Lavie, D. (2006). Capability Reconfiguration: An Analysis of Incumbent Responses to Technological Change. Academy of management review, 31(1), 153-174. DOI:

Lenz, R. T. (1981). ‘Determinants’ of Organizational Performance: An Interdisciplinary Review. Strategic Management Journal, 2(2), 131-154. DOI:

Lindsay, W. M., & Rue, L. W. (1980). Impact of the Organization Environment on the long-range Planning Process: A contingency view. Academy of Management Journal, 23(3), 385-404. DOI:

Ling, Y., Zhao, H., & Baron, R. A. (2007). Influence of Founder—CEOs' Personal Values on Firm Performance: Moderating Effects of Firm Age and Size. Journal of Management, 33(5), 673-696. DOI:

Lloret, A. (2016). Modeling Corporate Sustainability Strategy. Journal of Business Research, 69(2), 418- 425. DOI:

Mdolo, M. P., Naghavi, N., Fah, B. C. Y., & Jin, T. C. (2018). Corporate Sustainability Adoption Amongst Public Listed Companies in Malaysia. The Turkish Online Journal of Design, Art and Communication, 8, 509-517.

Mintzberg, H., & Waters, J. A. (1985). Of Strategies, Deliberate and Emergent. Strategic Management Journal, 6(3), 257-272. DOI:

Muhammad Kashif, S., Lai, F.-W., Fatt, C. L., Klemeš, J. J., & Bokhari, A. (2019). Integrating Sustainability Reporting into Enterprise Risk Management and Its Relationship with Business Performance: A Conceptual Framework. Journal of Cleaner Production, 208, 415-425. DOI:

Mulcahy, J. F. (1990, March). Management of the Building Firm. Joint Symposium on Building Economics and Construction Management, Sydney. DOI:

Nandakumar, M. K., Ghobadian, A., & O'Regan, N. (2011). Generic Strategies and Performance–Evidence from Manufacturing Firms. International Journal of Productivity and Performance Management. https://doi.org/DOI:

Omar, C. M. Z. C., & Azmi, N. M. N. (2015). Factors Affecting the Success of Bumiputera Entrepreneurs in Small and Medium Enterprises (SMEs) in Malaysia. International Journal of Management Science and Business Administration, 1(9), 40-45. DOI:

Othman, M. H. (2010). A Study on Problems of Bumiputera Contractor in Construction Industry Universiti Malaysia Pahang.

Panda, A. K. (2020). Firm Size & Sustainable Performance. Aegaeum Journal, 8(6), 943-958.

Pearce, J. A., Freeman, E. B., & Robinson Jr, R. B. (1987). The tenuous link between formal strategic planning and financial performance. Academy of Management review, 12(4), 658-675. DOI:

Pearce, J. A., & Robinson, R. B. (2009). Strategic Management: Formulation, Implementation, and Control (11th ed.). In B. Gordon (Ed.). McGraw-Hill/Irwin. https://books.google.com.my/books?id=4QoXAREhA9AC

Pertusa-Ortega, E. M., Zaragoza-Sáez, P., & Claver-Cortés, E. (2010). Can formalization, complexity, and centralization influence knowledge performance? Journal of Business Research, 63(3), 310-320. DOI:

Pitts, R. A., & Lei, D. (2000). Strategic Management: Building and Sustaining Competitive Advantage.

Porter, M. E. (1998). Competitive Strategy: Techniques for Analyzing Industries and Competitors. Free Press.

Rahman, I. A., & Rahmat, N. I. (2016). Causes of Failure Among Bumiputera Contractors. ARPN Journal of Engineering and Applied Sciences, 11(16). http://www.arpnjournals.org/jeas/research_papers/ rp_2016/jeas_0816_4854.pdf

Ramli, S. (2017). Syarikat Berkaitan Kerajaan Agen Memperkasakan Ekonomi [Government Related Companies Economic Empowerment Agents]. Dewan Ekonomi, Dewan Bahasa Dan Pustaka, 7-9.

Sabiu, I. T., Abdullah, A. A., & Amin, A. (2017). Impact of Motivation and Personality Characteristics on Bumiputeras’ Entrepreneurial Persistance in Malaysia. Journal of Developmental Entrepreneurship, 22(2), 13. DOI:

Serpell, A., Kort, J., & Vera, S. (2013). Awareness, Actions, Drivers and Barriers of Sustainable Construction in Chile. Technological and Economic Development of Economy, 19(2), 272-288. https://doi.org/DOI:

Shafii, F., Arman Ali, Z., & Othman, M. Z. (2006). Achieving Sustainable Construction in the Developing Countries of Southeast Asia. https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.603. 6965&rep=rep1&type=pdf

Shrivastava, P. (1995). The Role of Corporations in Achieving Ecological Sustainability. Academy of management review, 20(4), 936-960. DOI:

Sukur, K. M., Ahnuar, E. M., Rahman, N. A. A., & Zawawi, E. M. A. (2018). Challenges of Bumiputera Contractor in Malaysia Construction Industry. BiiDE2018, Pahang.

Tarifi, N. (2021). A Critical Review of Theoretical Aspects of Strategic Planning and Firm Performance. Open Journal of Business and Management, 9(4), 1980-1996. DOI:

Thomson, A., Strickland, A. J., & Gamble, J. E. (2001). Crafting and executing strategy. McGraw-Hill, 99, 100.

Yesil, S., & Kaya, A. (2013). The Effect of Organizational Culture on Firm Financial Performance: Evidence from a Developing Country. Procedia - Social and Behavioral Sciences, 81, 428-437. https://doi.org/DOI:

Yoon, J., & Suh, M.-G. (2019). Determinants Of Organizational Performance: Some Implications for Top Executive Leadership in Korean Firms. Asia Pacific Business Review, 25(2), 251-272. https://doi.org/DOI:

Zahid, M., & Ghazali, Z. (2017). Corporate Sustainability Practices and Firm's Financial Performance: The Driving Force of Integrated Management System. Global Business & Management Research, 9, 479-491.

Zainul Abidin, N. (2009). Sustainable Construction in Malaysia Developers' Awareness. Proceedings of World Academy of Science, Engineering, and Technology, 41, 807-814.

Zhang, M., Tse, Y. K., Doherty, B., Li, S., & Akhtar, P. (2018). Sustainable supply chain management: Confirmation of a higher-order model. Resources, Conservation and Recycling, 128, 206-221. DOI:

Copyright information

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

About this article

Publication Date

18 August 2023

Article Doi

eBook ISBN

978-1-80296-963-4

Publisher

European Publisher

Volume

1

Print ISBN (optional)

-

Edition Number

1st Edition

Pages

1-1050

Subjects

Multi-disciplinary, Accounting, Finance, Economics, Business Management, Marketing, Entrepreneurship, Social Studies

Cite this article as:

Binti Hussin, N. A., & Daud, S. (2023). Strategy Formulation and Sustainability Performance of Bumiputera Construction Companies: A Conceptual Paper. In A. H. Jaaffar, S. Buniamin, N. R. A. Rahman, N. S. Othman, N. Mohammad, S. Kasavan, N. E. A. B. Mohamad, Z. M. Saad, F. A. Ghani, & N. I. N. Redzuan (Eds.), Accelerating Transformation towards Sustainable and Resilient Business: Lessons Learned from the COVID-19 Crisis, vol 1. European Proceedings of Finance and Economics (pp. 409-419). European Publisher. https://doi.org/10.15405/epfe.23081.35